Complete Solaria (CSLR) Issues Update on Operational Progress & PE Debt

Tweet

Tweet Share

ShareGet Alerts CSLR Hot Sheet

Join SI Premium – FREE

Complete Solaria, Inc. (“Complete Solaria” or the “Company”) (Nasdaq: CSLR) today reported on its current financial status, which includes progress on its cash burn rate, and the status of its debt with private equity firms Kline-Hill Partners and Carlyle, which together hold about $70 million in debt owed on about $35 million of principal, split roughly equally between the two (see our 10K for exact numbers). First, we report on our progress in turning Complete Solaria (CSLR) around financially, starting with our dramatic headcount reduction from 428 to 109 (-74.5%) in seven rounds of layoffs.

These layoffs were very unfortunate, but necessary for survival. And when any company keeps only the top 25% of its employees, it winds up with an excellent workforce. Yesterday, our board approved 2.6 million stock options to retain those employees for the next five years and to reward them for their sacrifices. There has been a concomitant reduction in operating expense from $12,123,000 in Q1’23 (audited) to $5,655,000 this quarter (a company estimate from the 2024 plan1). With fewer people, we have been able to close down several buildings in California and to move our HQ to Salt Lake City, Utah, a solar center of excellence, where our costs are about 30% lower than those in California. Despite the reduction in workforce, we have seen a notable increase in employee productivity as well as improved business processes, better product quality and a significant increase in NPS score.

T.J. Rodgers, Complete Solaria chairman, commented, “In the conclusion of my November report to shareholders, I said:

‘Our planned future cash need is less than $5 million needed until mid-2024. Obviously, these estimates have high uncertainty in a company with immature business processes in the current chaotic market, but the company has become fundable by existing investors [i.e., me] with acceptable dilution.’

Rodgers continued, “Since that time, I have put $10 more million into CSLR to take my total investment to $68 million. Now, our current annual plan predicts that very little added investment will be needed this year. As of today, my personal breakeven CSLR market price is about $3.50. At a price of $3.50, our two private-equity debt holders would have 19.6 million shares worth $68 million, double their original $35 million investment – 100% profit, if they accepted our debt-equity swap proposal. This is the win-win deal that would make them money, save 109 jobs and clear a path for substantial CSLR equity value growth over time.”

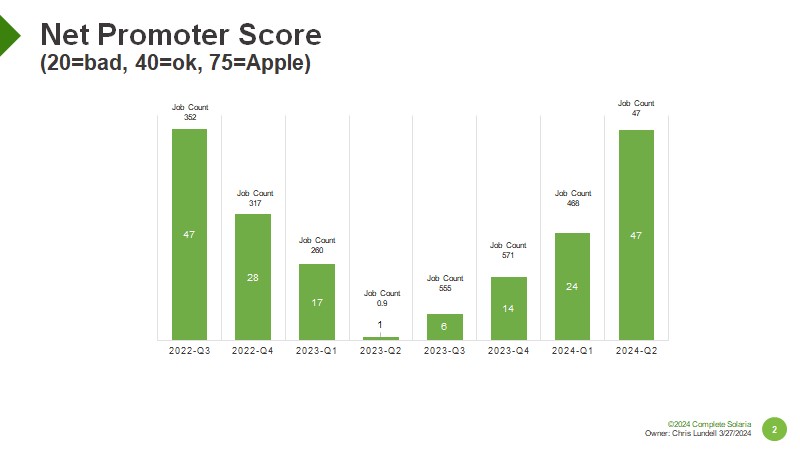

Rodgers continued, “Our operations group has reduced our cycle time from 104-133 days in the pre-Nov’23 period to 26-40 days today. Our customers have awarded that effort by raising our Net Promoter Score as shown below. We have also made significant progress in improving our attitude regarding customers.”

Rodgers continued, “Our proposition was compelling for Kline-Hill, always a supportive investor with whom we are in the final stages of negotiation of a debt-equity swap. Not so for Carlyle, which has rejected our equivalent 9.9 million share offer by complaining that they “have not heard back” from us on a day in which they dodged six phone calls and emails. The Carlyle story is long and does not reflect well on them, but we do owe them over $35 million which is delinquent. The problem is that they have used legal tactics to try to force every decision we make in an adverse direction and then use that threat as a club to demand that we divert critical funding to them. They once asked for half of the $10 million I was investing to keep the company alive, and another time demanded $10 million from me personally, or else they “would not go on.” That threat – made less than a week before our debt deal with them expired – caused me to think about life without Carlyle, a possibility completely under my control as long as I was willing to let them wipe out the common shareholders and auction off our net assets (less than $20 million, and hence another bad business decision).

Rodgers continued, “I have been working on CSLR for Carlyle for free for nine months – with no salary or stock options – and my prior Enphase turnaround results (from a share price of $0.92 in April 2017 to a share price of $115 today) are starting to show up, with all CSLR vital signs starting to point in the right direction (we still would have $20 million owed to lawyers and auditors, if successful). However, I’m not willing to work for Carlyle for free anymore – in fact, I’m not willing to work for Carlyle at all – ever again, for reasons I will detail in a separate press release. If they choose to take the equity we offer, I will finish the job I started for all shareholders. If they continue to demand the slavery of covenants, I will resign.

Rodgers concluded, “So, Carlyle’s threat to “not go forward” created a compelling vision of freedom for me, worth every penny I would lose. But, I would choose not to undermine their efforts because that’s too expensive. I wish them well. I will even come back for one week to train one of the solar hot-shots they claim to have in their broad solar portfolio – and leave him or her with 1) 110 great employees eager to make money on their new stock options, 2) a bank account of one million dollars, and 3) a credible zero-cash plan. They will have no need to force chapter 11 on us. I will leave the keys under the mat. Unfortunately, the 15 Ayna consultants I have helping me – the very same group that helped me turn around Enphase – are working for equity, rather than their usual $20 million fee. That will be the first problem facing the new Carlyle team.”

Serious News for Serious Traders! Try StreetInsider.com Premium Free!

You May Also Be Interested In

- Segro board minded to recommend Prologis's fourth takeover bid

- Hyliion wins $41.7M Navy contract for KARNO power systems

- FDA approves GSK lung cancer drug Jideytro ahead of schedule

Create E-mail Alert Related Categories

Corporate News, Guidance, Management CommentsRelated Entities

BankruptcySign up for StreetInsider Free!

Receive full access to all new and archived articles, unlimited portfolio tracking, e-mail alerts, custom newswires and RSS feeds - and more!